Fashion Ecommerce in the Netherlands: How Dutch Brands Are Growing Online

The Netherlands is the third-largest fashion ecommerce market in the Benelux - and it behaves very differently from Belgium and Germany. Dutch consumers are among the most digitally native in Europe, they return more than anyone else, and they expect fast delivery as a baseline requirement, not a premium.

For Dutch fashion brands trying to grow online, that creates a specific set of challenges. The market is competitive, returns eat into margin, and trust signals matter more than they do elsewhere. For brands from Belgium or Germany entering the Dutch market, the adjustments required are real - but so is the opportunity.

We work with fashion brands across Belgium, the Netherlands, and beyond. Here is what we have seen in the Dutch market - what is working, what is different, and what most brands underestimate when they try to scale here.

Key Takeaways

- •The Dutch fashion ecommerce market is highly competitive and return-driven - plan your margin accordingly before scaling ad spend.

- •Dutch consumers convert better on mobile than most European markets, but they also abandon cart faster if delivery options are limited.

- •Meta Ads work in the Netherlands, but creative strategy needs to be sharper - Dutch shoppers are ad-savvy and quick to scroll past generic creatives.

- •Email flows are underused by most Dutch fashion brands - this is one of the highest-leverage opportunities we see in the market.

- •If you are entering the Dutch market from Belgium, localise the experience: Dutch language and tone are non-negotiable.

The Dutch Fashion Ecommerce Landscape: What the Numbers Show

The Netherlands has a population of 18 million and one of the highest ecommerce penetration rates in Europe. Online fashion is the largest ecommerce category by volume, and Dutch consumers are comfortable buying across all price points online - from fast fashion to premium brands.

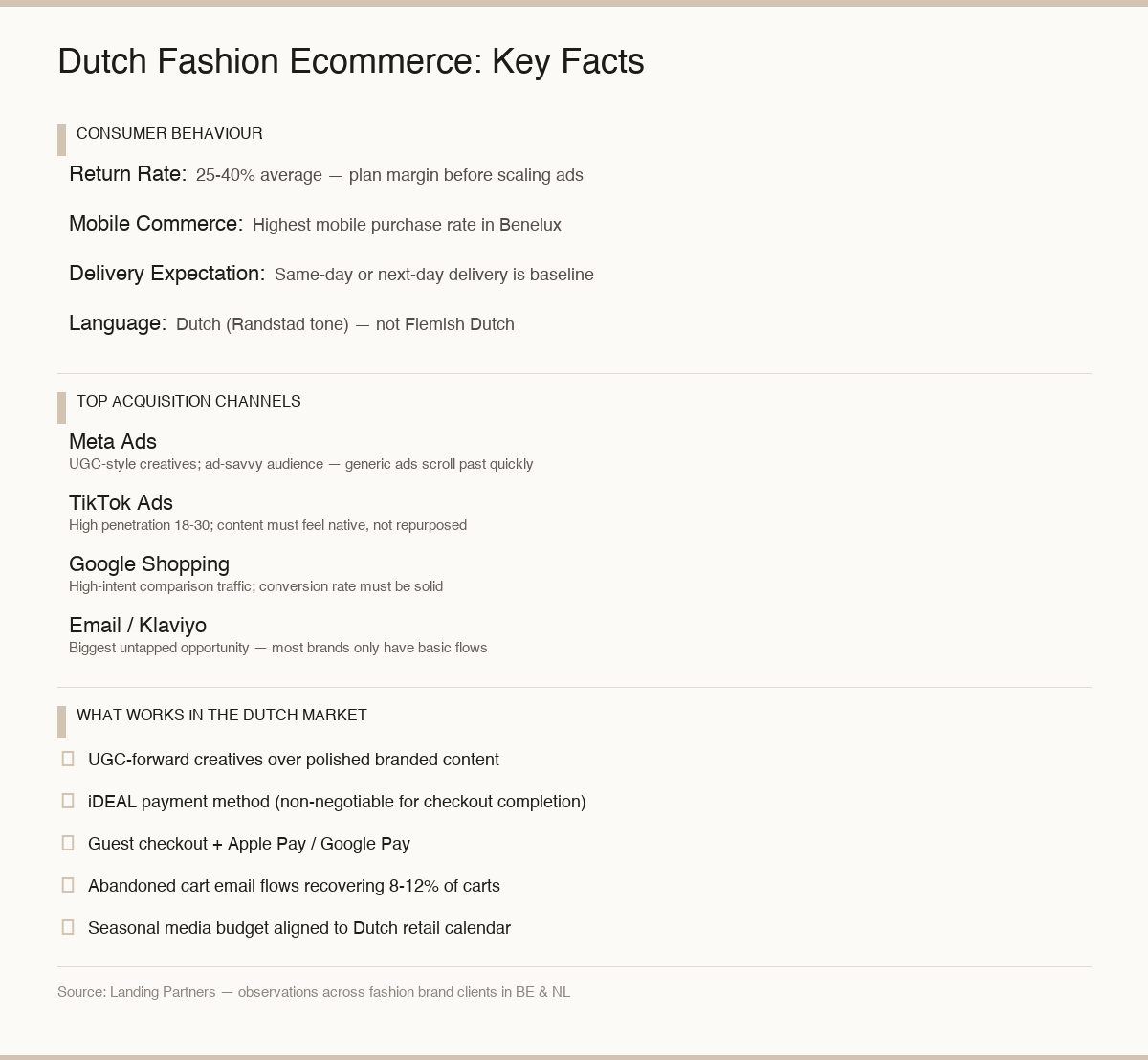

What is different here compared to most markets: **returns are treated as part of the shopping experience.** Dutch consumers return more frequently than Belgian, German, or French shoppers, and they expect returns to be free. If you are not accounting for a 25-40% return rate in your margin model when selling in the Netherlands, your unit economics will surprise you.

Dutch fashion ecommerce consumers return at rates 20-40% higher than Belgian or French shoppers. Free returns are not a differentiator - they are a baseline expectation that affects margin planning before you run a single ad.

The market is dominated by a few large players - Zalando, About You, and Wehkamp sit at the top - but there is a growing segment of Dutch consumers who actively prefer buying from independent brands. That preference is strongest in the 25-40 age group, where brand identity and story matter as much as product.

For independent fashion brands, the competition is not always Zalando. It is the 10-15 other DTC fashion brands in the same price segment that are now running sophisticated paid media campaigns in the Dutch market.

How the Dutch Consumer Differs from Belgian and German Shoppers

If you are a Belgian brand expanding to the Netherlands, do not assume the markets are interchangeable. The language is shared, but the consumer behaviour is not.

Delivery expectations

Dutch consumers expect same-day or next-day delivery as standard. Belgium has caught up significantly, but in the Netherlands, even 2-day delivery increases cart abandonment. This is not an advertising problem - it is a logistical decision you need to solve before you scale paid traffic.

Price sensitivity and research behaviour

Dutch consumers are willing to spend, but they research more than Belgian shoppers. Price comparison behaviour is higher. If you are running a premium fashion brand, the emphasis on quality, materials, and brand story in your creatives needs to be stronger. **Discounting to compete is a short-term fix that damages brand equity in the long run.**

Language and tone

Dutch copy cannot be a direct translation of Belgian Dutch - the tone is different. Belgian Dutch tends to be more formal and measured; Dutch Dutch (particularly in the Randstad) is more direct, faster-paced, and less formal. This applies to ad copy, email subject lines, and website copy alike.

We have seen conversion rates improve meaningfully for Belgian brands entering the Netherlands once they adapted their copy tone - not just the language.

Brands that use generic Flemish copy for Dutch audiences convert 15-20% worse than brands that adapt tone specifically for the Dutch market. Localisation is not just translation - it is register.

Which Channels Drive Fashion Sales in the Netherlands

Meta Ads (Instagram and Facebook) remain the primary acquisition channel for fashion brands in the Netherlands. The market has high Instagram usage among the 18-40 demographic, and visual fashion content performs well. The challenge is not reach - it is cutting through.

Meta Ads

Dutch consumers are ad-savvy. Click-through rates for generic product ads are lower here than in Belgium. What works: authentic creatives, UGC-style video, strong visual hooks in the first two seconds, and copy that does not try too hard. Dutch shoppers respond to confidence and directness, not marketing speak. Your creative strategy needs to be sharper here than in most other European markets.

TikTok Ads

TikTok penetration in the Netherlands is high, especially in the 18-30 segment. For streetwear, sportswear, and trend-led fashion brands, TikTok is an underused acquisition channel. The creative requirements are different from Meta - content needs to feel native to the platform, not repurposed from Instagram.

Google Shopping

For fashion brands with a solid product feed and competitive pricing, Google Shopping drives high-intent traffic. Dutch consumers use Google to compare before purchasing. If your product pages are not converting that traffic, the channel will underperform - it is a conversion rate problem, not a media problem.

Email Marketing

This is where we see the biggest untapped opportunity in the Dutch market. Most Dutch independent fashion brands run basic email setups - a welcome email and a promotional campaign calendar. The brands that do email well, with complete Klaviyo flow architecture, proper segmentation, and lifecycle-based sends, are meaningfully ahead of most competitors.

Building an email list is the most durable asset a Dutch fashion brand can build. It is not subject to algorithm changes, platform cost increases, or ad auction dynamics. **If you are running paid media in the Netherlands without a full retention stack behind it, you are acquiring customers you do not keep.**

Not sure how your current setup would perform in the Dutch market? Book a free growth call - we will review your channels and tell you exactly what needs to adapt for the Netherlands.

What Dutch Fashion Brands Are Getting Right Online

The Dutch brands that are scaling online share a few common traits we see consistently across our client base and in the brands we audit.

Strong brand identity before paid media scale

The Dutch brands growing fastest have invested in a clear visual identity before scaling paid spend. Product quality is assumed. What differentiates them is how they communicate - the story, the aesthetic consistency, the sense of who the brand is for. Paid media amplifies this; it does not create it.

Mobile-first execution throughout the funnel

The Netherlands has one of the highest mobile commerce rates in Europe. **If your product pages, checkout flow, and ad creatives are not optimised for mobile, you are losing revenue at every step of the funnel.** This is a prerequisite for running paid media profitably, not an optional improvement.

Return rate management built into the model

The brands that thrive in the Dutch market have structured their pricing and margin model to absorb returns. They do not fight returns - they plan for them. This changes how they approach free shipping thresholds, sizing guidance, and product photography investment.

Brands that include explicit size guides, flat lay product photos, and model measurements on product pages see return rates 10-15% lower than average. At scale, that margin improvement is material.

What We Have Seen Working in the Dutch Market

Based on our work with fashion brands across Belgium and the Netherlands, these are the patterns that consistently move the needle.

UGC-forward creatives outperform branded content

Dutch consumers trust peer reviews and authentic content more than polished brand photography. For Meta and TikTok ads, UGC-style video - real customers, natural environments, genuine reactions - tends to outperform studio shoots. This does not mean low quality. It means honest. The brands that understand this distinction win the Dutch market on paid social.

Fast checkout is a direct conversion lever

Dutch shoppers abandon cart faster than Belgian shoppers when checkout is slow or has too many steps. Enabling iDEAL (the dominant Dutch payment method), Apple Pay, and a guest checkout option is not optional - it is a measurable conversion improvement. Every checkout step you remove increases completion rate.

Email flows recover a meaningful share of abandoned carts

Fashion brands in the Netherlands with a well-structured abandoned cart flow recover 8-12% of abandoned carts on average. Most Dutch brands we audit do not have this fully in place. If you are running paid traffic to your store and not recovering that abandonment with email automation, you are leaving acquired revenue on the table every day.

Seasonal timing follows Dutch retail rhythms

Dutch fashion retail has specific seasonal beats that differ from the Belgian calendar. January sales, the spring collection launch in February-March, summer sale in July, and BFCM in November are the key commercial moments. **Brands that plan their media budget and creative calendar around these moments outperform brands that run a flat spending curve year-round.**

How to Enter the Dutch Market as a Fashion Brand

If you are a Belgian brand moving into the Netherlands, or a Dutch brand trying to professionalise your online operation, the sequencing matters.

First: fix the fundamentals. Dutch copy, iDEAL payment, clear return policy, delivery time prominently displayed. These are pre-conditions - not growth levers. You cannot grow in the Netherlands without them.

Second: build your email foundation before scaling paid media. A welcome series, abandoned cart flow, and post-purchase sequence should be in place before you push volume into the funnel. Email is cheaper than paid acquisition, and it retains the customers your paid media acquires.

Third: test your creative before scaling. The Dutch market rewards honest, visual storytelling. Run a small test budget, identify what resonates, then scale what works. Do not bring your Belgian or German creatives to the Dutch market unchanged.

For brands at an earlier stage, the most important question is not which channel to add - it is whether the store converts the traffic it already has. **A store that does not convert organically will not be fixed by advertising.** This is true everywhere, but it is more costly to ignore in the Netherlands where CPMs are higher than the Belgian market.

Every brand's situation is different. Growing in the Dutch market depends on your margin, your current setup, and what stage you are in. If you want to know what the right next step looks like for your specific brand, book a free growth call.

The Dutch Competitive Landscape: What to Expect

The Netherlands attracts fashion brands from across Europe. You will be competing not just with Dutch DTC brands, but with Belgian, German, and Scandinavian brands that have localised for the Dutch market.

In the mid-market fashion segment (60-150 AOV), competition in Dutch Meta auction is meaningful. CPMs in the Netherlands are higher than in Belgium on average - which means your creative quality and landing page conversion rate need to be stronger to maintain a profitable ROAS.

In the premium segment (150+ AOV), the Dutch market is less saturated than Germany or the UK. There is genuine opportunity for a well-positioned brand with a clear identity to build a loyal customer base here.

The brands that struggle in the Netherlands share one trait: they entered the market without adapting the experience. Same creatives, same copy, same checkout - just with a Dutch postal code filter on their Meta ads. That approach does not work. **The Dutch market rewards brands that take it seriously enough to adapt every layer of the funnel.**

Frequently Asked Questions

Growing a fashion brand in the Netherlands is a real opportunity - but one that rewards preparation. The market is digital, competitive, and unforgiving of shortcuts. Brands that adapt the experience, plan for returns, and invest in email alongside paid media are the ones we see building durable growth here.